Bank vs. Alternative Lenders: Finding Your Perfect Funding Match?

In my years analyzing the fintech and business lending space, I’ve seen countless entrepreneurs face the same daunting crossroad. You’ve built a solid business, you have a vision for growth, but you need capital to make it happen. The problem? The world of business financing has become a dizzying landscape of choices. On one side stands the traditional bank, a symbol of stability but often perceived as slow and rigid. On the other, the burgeoning world of alternative lenders, promising speed and flexibility but sometimes at a confusing and costly premium.

You’re likely wrestling with this very dilemma. You’ve probably heard horror stories of month-long bank application processes ending in rejection, and you might be wary of the high interest rates associated with fast online loans. This uncertainty is more than just a headache; it’s a barrier to growth. Making the wrong choice can mean paying thousands in unnecessary interest, getting locked into unfavorable terms, or worse, missing a critical business opportunity while waiting for funding.

This is where the noise stops. This guide will provide the clarity you need, breaking down the essential differences between banks and alternative lenders. We won’t rely on guesswork or outdated advice. Instead, we’ll dive deep into the latest data from top-tier government and industry sources, giving you the power to make a truly informed, strategic decision for your business’s future. We’ll cover the evolving landscape of lending in 2025, conduct a head-to-head comparison of your options, and walk you through a step-by-step guide to finding your perfect funding match.

The Evolving Landscape of Small Business Lending in 2025

The way businesses access capital has fundamentally shifted. The once-linear path to a local bank manager’s office has splintered into a dozen different digital avenues. Here’s the thing: understanding this new environment is the first step to navigating it successfully.

Post-Pandemic Entrepreneurship and the Shifting Demand for Capital

The post-pandemic economy has created a unique dynamic. While entrepreneurship is booming, the financial environment has become more challenging. According to ZING Funding’s review of 2024, the year was characterized by high interest rates and cautious lending policies from traditional institutions. In fact, data from the Federal Reserve Bank of Kansas City shows that credit standards tightened for the thirteenth consecutive quarter in late 2024. This caution from banks has pushed many business owners to explore other avenues.

The Unstoppable Rise of Fintech and Digital-First Lending

This is where fintech swoops in. The growth of financial technology has, as experts at Asymmetric Marketing put it, “dramatically changed the small business financing landscape.” This isn’t just a minor trend; it’s a seismic shift. The digital lending market, which was valued at $11.6 billion in 2021, is forecasted to explode to $48.3 billion by 2029, according to Fortune Business Insights (cited by Highen Fintech). This growth is fueled by a demand for what traditional banking often lacks: speed, accessibility, and innovation.

Key Lending Trends to Watch: AI, Embedded Finance, and Personalization

Looking ahead, the experts at Highen Fintech predict that “The digital lending ecosystem is expected to undergo rapid development in 2025.” What does this mean for you?

- AI-Driven Underwriting: Forget weeks of waiting. According to McKinsey & Company (cited by Highen Fintech), AI can improve loan processing time by a staggering 70% to 80%.

- Embedded Lending: Expect to see financing options directly embedded within the software you already use (think getting a loan directly from your accounting or payment processing platform). Defacto predicts this market will grow from $7.65 billion in 2024 to $45.74 billion by 2034.

- Challenger Banks: Digital-only banks are becoming serious players. The “neo and challenger bank” market was valued at $69.6 billion in 2024, and it’s not slowing down. Take Chime, for example; its customer base grew from 14.5 million in 2022 to 22.3 million in 2024, according to a report by FinTech Insights.

![[INFOGRAPHIC: A timeline showing the key milestones in the growth of fintech lending from 2015 to a projected 2029, highlighting the market value growth from sources like Fortune Business Insights.]](https://7tops.com/wp-content/uploads/2025/09/aaa-1-300x300.png)

Traditional Banks: The Bedrock of Business Financing

Even with the fintech revolution, traditional banks remain a cornerstone of the economy. From my perspective, dismissing them would be a major mistake for the right kind of business. They are the established, regulated institutions that have fueled business growth for centuries.

What Do Banks Offer?

Banks typically provide a suite of core financing products:

- Term Loans: A lump sum of cash paid back over a set term. Ideal for large, one-time investments like purchasing equipment or real estate.

- Business Lines of Credit: A revolving credit line you can draw from as needed, perfect for managing cash flow or unexpected expenses.

- SBA Loans: Loans partially guaranteed by the U.S. Small Business Administration, which reduces the bank’s risk and can lead to better terms for the borrower.

- Commercial Real Estate Loans: Specialized loans for purchasing or renovating business properties.

The Pros of Banking with a Traditional Lender

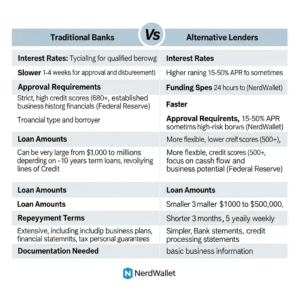

The biggest draw? The cost. “Average bank loan interest rates typically range from 6.6% to 11.5%,” according to September 2025 data from NerdWallet. This is significantly lower than most alternative options. Beyond rates, building a relationship with a bank can offer integrated services like business checking, credit cards, and treasury management.

The Cons of Traditional Bank Loans

Here’s the tradeoff. Banks are notoriously risk-averse. The application process is lengthy and requires extensive documentation. Their approval criteria are strict, often demanding high credit scores, years of business history, and significant collateral. This reality is reflected in the data: a 2023 report from the Federal Reserve found that while small banks approved 75% of applicants for at least some financing, larger banks only approved 66%. If you’re a startup or have less-than-perfect credit, the odds can be stacked against you.

Who is the Ideal Candidate for a Bank Loan?

You’ll thrive with a bank loan if your business has:

- A strong track record: At least 2-3 years in operation.

- Excellent credit: Both personal and business credit scores are high.

- Solid financials: Demonstrable profitability and healthy cash flow.

- Collateral: Assets like real estate or equipment to secure the loan.

- Patience: You don’t need the capital immediately.

The New Guard: A Deep Dive into Alternative Lenders

If banks are the bedrock, alternative lenders are the dynamic, fast-moving disruptors building on top of it. This category is broad, encompassing everything from sophisticated online lenders to specialized financing companies.

Who Are Alternative Lenders?

This isn’t a monolith. The term “alternative lender” includes:

- Online Lenders: Fintech platforms that use technology for underwriting and funding (e.g., OnDeck, Kabbage).

- Invoice Factoring Companies: Businesses that purchase your outstanding invoices at a discount, providing immediate cash flow.

- Merchant Cash Advance (MCA) Providers: Companies that offer a lump sum in exchange for a percentage of your future sales.

- Peer-to-Peer (P2P) Lenders: Platforms that connect businesses with individual investors.

The Pros of Choosing an Alternative Lender

The primary advantage is speed. While a bank loan can take months, many online lenders can approve and fund a loan in as little as 24-48 hours. They are also significantly more flexible with their eligibility criteria, often approving businesses with lower credit scores, shorter operating histories, and no collateral. Their higher approval rates are a major draw for those who can’t meet the stringent requirements of traditional banks.

The Cons of Alternative Lending

That speed and flexibility come at a price. According to NerdWallet’s 2025 data, interest rates from online lenders can range from 14% to a jaw-dropping 99% for products like MCAs. Repayment terms are often much shorter, which can strain cash flow. Furthermore, the industry is less regulated than traditional banking, meaning you need to be extra vigilant about reading the fine print and understanding all fees. I believe the biggest mistake I see business owners make here is focusing only on the speed without fully calculating the total cost of the loan.

Who Should Consider an Alternative Lender?

An alternative lender might be your perfect match if your business:

- Needs cash urgently: To seize an opportunity or cover an emergency expense.

- Is a startup or young business: Without the multi-year history banks require.

- Has a lower credit score: Or a recent blemish on your credit report.

- Lacks significant collateral: To secure a traditional loan.

- Has been rejected by a bank: And needs another path to funding.

Head-to-Head Comparison: Banks vs. Alternative Lenders

Let’s break it down feature by feature to see how these two options stack up against each other. What I wish someone had told me early in my career is that it’s not about “good” vs. “bad” but “right fit” vs. “wrong fit.”

Interest Rates & Total Cost: A Tale of Two Models

As we’ve seen, banks offer lower rates (6.6%-11.5%) while alternatives are higher (14%-99%), as documented by NerdWallet. But it’s crucial to look beyond the interest rate to the Annual Percentage Rate (APR), which includes all fees. Some alternative products, like Merchant Cash Advances, use a “factor rate” which can be misleadingly low until converted to an APR. Always calculate the total cost of capital before signing.

Application and Funding Speed: The Need for Speed

There’s no contest here. Alternative lenders win on speed, hands down. Their streamlined, tech-driven online applications can lead to funding in 1-3 business days. Banks, with their manual underwriting and multi-level approval processes, can take anywhere from 30 to 90 days.

Eligibility and Approval Rates: Who Gets the Green Light?

The Federal Reserve’s 2023 report provides a clear picture: banks are more selective. Credit unions, another traditional option, fully approved 51% of applicants. The approval rates for online lenders are generally higher because their models are built to take on more risk, often using different data points (like daily sales data) to assess creditworthiness.

Loan Amounts and Terms: Finding the Right Fit

Banks are typically better suited for large, long-term financing needs, such as multi-million dollar commercial real estate loans with 10-25 year terms. Alternative lenders shine in the small-to-medium loan space, offering amounts from a few thousand dollars up to around $500,000, with much shorter repayment terms, often between 6 and 24 months.

The Role of Government and Regulation in Business Lending

It’s easy to get lost in the private sector options, but the government plays a huge role in the small business lending ecosystem.

The SBA’s Impact on the Lending Landscape

The Small Business Administration doesn’t lend money directly; it guarantees a portion of loans made by approved lenders (mostly banks). This guarantee makes it less risky for the bank, which can lead to lower rates and longer terms than they might otherwise offer. The SBA’s impact is massive. In Fiscal Year 2023, the agency approved over 63,000 loans through its main programs, totaling nearly $34 billion, according to Bankrate. And that activity is growing; Canopy Servicing notes a 22% increase in the number of approved SBA loans in 2024 compared to 2023.

How the CFPB and Treasury Protect Small Business Borrowers

As alternative lending grows, so does the need for oversight. The Consumer Financial Protection Bureau (CFPB) provides resources and education for business owners. Additionally, government initiatives like the State Small Business Credit Initiative (SSBCI) are making a real difference. A November 2024 report from the U.S. Department of the Treasury showed the SSBCI has already supported $3.1 billion in new financing for over 3,600 small businesses. I find it particularly interesting that 75% of these transactions supported underserved businesses, demonstrating a commitment to equitable access to capital. As U.S. Deputy Secretary of the Treasury Wally Adeyemo stated, “Small businesses and hard-working entrepreneurs are at the core of the American economy and supporting them has been a central priority.”

Making the Right Choice: A Step-by-Step Guide

So, how do you synthesize all this information and make a decision? Let’s walk through a practical framework.

- Assess Your “Why” and “When”: Why do you need the money? Is it for a long-term investment (buy a building) or a short-term need (cover a cash flow gap)? When do you need it? Next quarter or next week? Your answers here are your first filter.

- Conduct a Brutally Honest Financial Self-Audit: What is your credit score? How long have you been in business? What are your annual revenues? What collateral can you offer? Be realistic. This will tell you which doors are likely open to you.

- Gather Your Documentation: Get your financial house in order before you apply. This includes bank statements, tax returns, a solid business plan, and profit & loss statements. Being prepared can dramatically speed up the process, even with alternative lenders.

- Compare, Compare, Compare: Never take the first offer. Get quotes from at least one traditional bank, one SBA lender, and two different types of alternative lenders. Lay out the APR, total repayment amount, and terms side-by-side to understand the true cost.

FAQ: Your Top Questions Answered

What is the main difference between a bank and an alternative lender?

The primary differences are speed, cost, and eligibility. Banks are generally slower and have stricter requirements but offer lower interest rates. Alternative lenders are faster and more flexible but typically come with higher costs.

Are alternative lenders more expensive than banks?

Yes, in almost all cases. Data from NerdWallet shows a clear gap, with bank rates often in the single digits while alternative lender rates start in the double digits and can go much higher.

How quickly can you get a loan from an alternative lender?

Many online lenders can provide funding within 24 to 72 hours of a completed application, a key advantage over the 30-90 day timeline common with traditional banks.

Why would a business choose an alternative lender over a traditional bank?

Common reasons include the need for fast funding, a credit score or business history that doesn’t meet bank standards, a lack of collateral, or having been previously denied by a bank.

Are online lenders safe and legitimate?

The majority are, but it’s a less-regulated industry. Look for lenders with a strong track record, positive reviews on sites like Trustpilot, and transparent terms. Always verify their physical address and contact information.

Conclusion: Your Funding, Your Choice

Navigating the choice between a bank and an alternative lender isn’t about finding a universally “better” option; it’s about finding the one that’s strategically right for your business, right now.

Let’s boil it down:

- Banks are your go-to for low-cost, long-term capital if you have a strong financial profile and the time to navigate their process.

- Alternative lenders are your powerful ally for speed and accessibility, providing a vital lifeline for startups, businesses needing fast cash, or those who don’t fit the traditional banking mold.

- The landscape is constantly evolving, with technology like AI making lending faster and government programs like the SBA and SSBCI creating more opportunities.

The power is now in your hands. You’re armed with the data, you understand the tradeoffs, and you have a framework for making a smart decision. The next step is to take action. Use the guide above to assess your business needs, and begin exploring the lenders that align with your specific goals. Choosing the right funding partner is one of the most critical decisions you’ll make, and it’s the fuel that will drive your business forward into 2025 and beyond.