Navigating the world of commercial mortgages can feel like trying to solve a Rubik’s Cube in the dark. The stakes are high, the terminology is dense, and a single misstep can cost you your dream property. In fact, the sheer scale of the market is staggering; total commercial real estate mortgage borrowing is projected to hit $583 billion in 2025, a significant 16 percent increase from 2024, according to a forecast by the Mortgage Bankers Association. You’re not just applying for a loan; you’re stepping into a massive, complex financial ecosystem.

The pain point for so many investors and business owners is a feeling of being completely overwhelmed. You’re left wondering: Am I getting a good rate? Is my paperwork strong enough? What are lenders really looking for? This uncertainty can be paralyzing.

In my 15 years of experience guiding clients through this exact process, I’ve seen firsthand how a little bit of insider knowledge can completely change the game. This guide is designed to give you that knowledge. We will demystify the entire commercial mortgage process, from understanding the core loan types to navigating the unforgiving underwriting process. I’ll provide you with a clear roadmap, backed by the latest industry data and real-world case studies, to help you secure the commercial property financing you need.

Here’s what we’ll cover:

- The Fundamentals: What a commercial mortgage is and how it fundamentally differs from a residential loan.

- The Loan Arsenal: A breakdown of the primary types of commercial property loans available.

- The Lender’s Gauntlet: What underwriters truly care about—the numbers and metrics that make or break a deal.

- The 2025 Market: A data-driven look at current rates, trends, and what to expect in the coming year.

- Real-World Success Stories: Actionable lessons from actual commercial mortgage case studies.

Let’s crack this maze together.

What is a Commercial Mortgage and Who is it For?

At its core, a commercial mortgage is a loan secured by a commercial property, rather than a residential one. Think office buildings, retail shops, industrial warehouses, apartment complexes, or even a mixed-use property. Unlike the standardized world of home loans, business mortgages are highly customized financial instruments.

The biggest mistake I see new investors make is assuming the process is similar to buying a home. It’s not. Here’s the key difference: a residential mortgage is underwritten based on your personal ability to repay the debt. A commercial mortgage, on the other hand, is primarily underwritten based on the property’s ability to generate income and cover its own debt. The lender is essentially investing in your business plan for that property.

Who needs a commercial mortgage?

- Business Owners: Companies looking to purchase their own premises, like an office, storefront, or factory, instead of leasing.

- Real Estate Investors: Individuals or firms buying income-producing properties, such as apartment buildings, shopping centers, or industrial parks.

- Developers: Those who need commercial construction loans to build properties from the ground up before converting to a permanent mortgage.

The Core Types of Commercial Mortgages Explained

There’s a whole alphabet soup of commercial real estate financing options. Choosing the right one depends entirely on your property type, financial situation, and long-term goals.

Traditional Commercial Mortgages

These are your bread-and-butter loans from banks and credit unions. They typically offer competitive rates but come with stringent qualification requirements. From my perspective, this is the best route for established borrowers with strong financials and a straightforward property purchase.

SBA Loans: 7(a) and 504 Programs

The Small Business Administration (SBA) doesn’t issue loans directly but guarantees a portion of the loan, reducing the risk for lenders. This makes it easier for small businesses to qualify.

- SBA 7(a) Loan: Can be used for a variety of business purposes, including real estate.

- SBA 504 Loan: Specifically designed for purchasing fixed assets like real estate and equipment, often with a lower down payment.

Conduit/CMBS Loans

Commercial Mortgage-Backed Securities (CMBS), or conduit loans, are commercial real estate loans that are bundled together and sold to investors on a secondary market. They often offer fixed rates and non-recourse options (meaning the lender can’t go after your personal assets in a default), but they are less flexible and come with stiff prepayment penalties.

Bridge and Hard Money Loans

Think of these as short-term solutions.

- Bridge Loans: “Bridge the gap” between an immediate financing need and a long-term solution. Perfect for repositioning a property or when you need to close fast.

- Hard Money Loans: A type of short-term, asset-based loan where the property itself is the primary collateral. Rates are much higher, but funding is fast and based less on creditworthiness. Use these with extreme caution.

The Gauntlet of Qualification: What Lenders Really Want to See

Here’s the thing about lenders: they are fundamentally in the business of managing risk. Your application’s job is to convince them that you are a safe bet. They do this by scrutinizing two key financial metrics above all others.

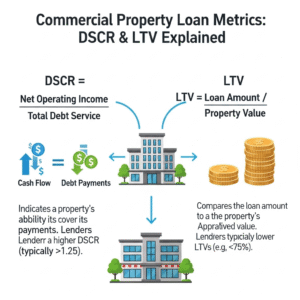

1. Debt Service Coverage Ratio (DSCR)

This is the single most important number in your application. It measures the property’s annual Net Operating Income (NOI) against its total annual mortgage debt service (principal and interest payments).

Formula: DSCR = Net Operating Income / Total Debt Service

A DSCR of 1.0x means the property generates exactly enough income to cover its mortgage payments. Lenders want to see a cushion. Most lenders require a minimum DSCR of 1.25x or higher. This tells them that even if your income dips or expenses rise, the property can still comfortably cover its debt.

2. Loan-to-Value (LTV) Ratio

LTV measures the loan amount against the appraised value of the property. It represents the lender’s stake in the deal.

Formula: LTV = Loan Amount / Appraised Property Value

If you’re buying a $1 million property and the lender offers a loan for $700,000, your LTV is 70%. This means you need to come up with a 30% down payment. Typically, commercial mortgage LTVs range from 65% to 80%, which is significantly lower than residential loans.

What I wish someone had told me early in my career is that these two numbers tell a story. A high DSCR and a low LTV signal a healthy, profitable property and a well-capitalized borrower—a story every lender wants to hear.

Assembling Your Application: A Step-by-Step Checklist

Being unprepared is the fastest way to get a “no” from a lender. You’ll need a comprehensive package that paints a complete picture of you, your business, and the property.

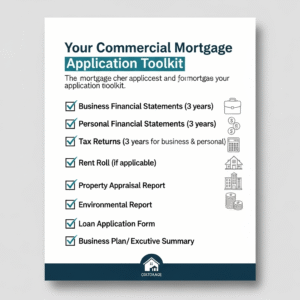

Your Essential Document Checklist:

- Personal Financial Statements: Detailed statements for all individuals owning 20% or more of the business.

- Business Financial Statements: At least three years of profit & loss statements, balance sheets, and tax returns.

- A Detailed Business Plan: Especially for owner-occupied properties, this should outline your company’s history, market, and growth projections.

- Property Information: A detailed description of the property, its operating history, current rent roll (if applicable), and a list of major tenants.

- Purchase Agreement: The signed contract to purchase the property.

- Appraisal and Environmental Reports: The lender will order these, but having recent reports can be helpful.

The Underwriting Deep Dive: Behind the Lender’s Curtain

Once you submit your application, it goes to the underwriter. Their job is to perform due diligence and verify every single piece of information you’ve provided. Look, let’s be honest, this part of the process can feel intrusive. They will scrutinize your credit history, your bank statements, and the property’s financial performance. The typical timeline from application to closing can range from 45 to 90 days, sometimes longer for complex deals.

Navigating the Current Commercial Mortgage Landscape (2024-2025)

The commercial real estate market is in a fascinating state of flux. After a period of uncertainty, we’re seeing a rebound in lending activity. The CBRE Lending Momentum Index, which tracks loan closings, saw a significant 37% year-over-year increase in late 2024, signaling a strong recovery.

However, challenges remain. A September 2024 report from the U.S. Government Accountability Office (GAO) noted that outstanding commercial real estate loans held by banks doubled to about $3 trillion between 2012 and 2024. The same report highlighted that delinquency rates, while still historically low, peaked at about 1.2 percent in late 2023, the highest since 2015.

What does this mean for you? It means lenders are open for business, but they are also cautious. This sentiment is echoed by industry leaders. James Millon, U.S. President of Debt & Structured Finance at CBRE, stated in a February 2025 release, “Looking ahead to 2025, we expect a more dynamic refinancing and investment sales market, fueled by maturing debt… and strong fundamentals across most real estate sectors.” [Source: CBRE]

Interest rates remain a central topic. While the Federal Reserve has been cautious, a September 2024 Deloitte outlook projected four more rate cuts in 2025, with the federal funds rate potentially settling around 4.5%. For borrowers, this suggests a potential for more favorable borrowing costs as the year progresses. However, don’t expect a return to the rock-bottom rates of the past. As Taylor Stork, Chief Operating Officer at Developers’ Mortgage, astutely noted, “Where we are today is a normalized interest rate environment.” [Source: Basecap Analytics]

Real-World Scenarios: Case Studies in Commercial Mortgages

Theory is one thing; practice is another. Let’s look at how these principles play out in the real world.

Case Study 1: Overcoming a Rolling Lease to Expand

- Scenario: Experienced investors wanted to refinance two properties to free up capital for expansion.

- The Challenge: One key property had a rolling lease, which made traditional lenders nervous about future income stability.

- The Solution: According to a case study by ABC Finance Ltd, a broker negotiated a deal with a prime lender by highlighting the long, stable history of the tenants. The result was a £344,250 loan on a £620,000 valuation, allowing the clients to expand their portfolio.

Case Study 2: Purchasing Premises and Slashing Overhead

- Scenario: Two business owners were renting their premises and had an opportunity to buy it from their landlord at a discount.

- The Challenge: Most lenders would only offer a 70% LTV, leaving a significant funding gap.

- The Solution: As detailed by Mortgage Corp, a broker sourced a lender willing to extend an 80% LTV loan. The new monthly mortgage payment of $4,700 was nearly $2,000 less than their previous rent, a massive win for their bottom line.

Case Study 3: Financing a Hotel Purchase with Creative Structuring

- Scenario: A couple with hotel experience was buying a 32-bed hotel but was delayed in selling a residential property needed for the down payment.

- The Challenge: The timing mismatch put the entire hotel purchase at risk.

- The Solution: A case study from How We Have Helped shows how a commercial finance consultant arranged a primary mortgage for 70% of the hotel’s value, and then secured a short-term bridging loan against the unsold flat to cover the rest. The bridging loan was paid off two months later when the flat sold, saving the deal.

These examples show that persistence, preparation, and often, the help of a knowledgeable broker can overcome significant hurdles.

Frequently Asked Questions (FAQ)

1. What is a good commercial loan rate?

Rates vary widely based on the loan type, property, and your financial strength. As of September 2025, rates can range from 6-8% for bank loans and SBA loans to over 10% for hard money loans, according to data from sources like Janover.

2. What is the typical down payment for a commercial mortgage?

Expect to put down between 20% and 35% of the purchase price.

3. What is the difference between a commercial and residential mortgage?

Commercial mortgages are based on the property’s income potential, have shorter terms (often 5-20 years), and require a larger down payment. Residential mortgages are based on your personal income and have longer terms (typically 30 years).

4. Can I get a commercial mortgage with bad credit?

It’s difficult but not impossible. You will likely need to work with non-traditional lenders, such as hard money lenders, and expect to pay a much higher interest rate and provide a larger down payment.

5. How long does it take to get a commercial mortgage?

The process typically takes 45 to 90 days from application to closing, but it can be longer for more complex transactions.

Conclusion: Your Path to a Successful Closing

The commercial mortgage maze, while complex, is not unsolvable. The key is understanding that you’re not just asking for money; you’re presenting a business case. Your success hinges on your ability to prove that your property is a sound investment capable of generating enough income to cover its debts and then some.

Here are your key takeaways:

- Know Your Numbers: Master your DSCR and LTV. These are the metrics that will make or break your application.

- Preparation is Paramount: Assemble a flawless, comprehensive application package before you approach lenders.

- Understand the Market: Be aware of current trends in interest rates and lending standards to set realistic expectations.

- Seek Expert Guidance: Don’t be afraid to work with a reputable commercial mortgage broker who can connect you with the right lenders for your specific scenario.

The journey to securing a commercial property loan is a marathon, not a sprint. But by being prepared, knowledgeable, and persistent, you can successfully navigate the process and unlock the financing needed to achieve your real estate goals. The next step is to take this knowledge and turn it into action. Start by organizing your financial documents and building your business case today.